February 2026 marks a clear shift for pricing in the UK fast-food sector, rises persist, while consumer demand weakens. Traffic fell by 1.5% year on year, even as overall prices increased from 7.7% in January to 8.2% in February.

More than half of the leading brands recorded declining performance, while only 37% achieved growth. Where growth did occur, it was largely driven by expansion rather than stronger underlying demand, particularly among chicken, coffee and American-led concepts.

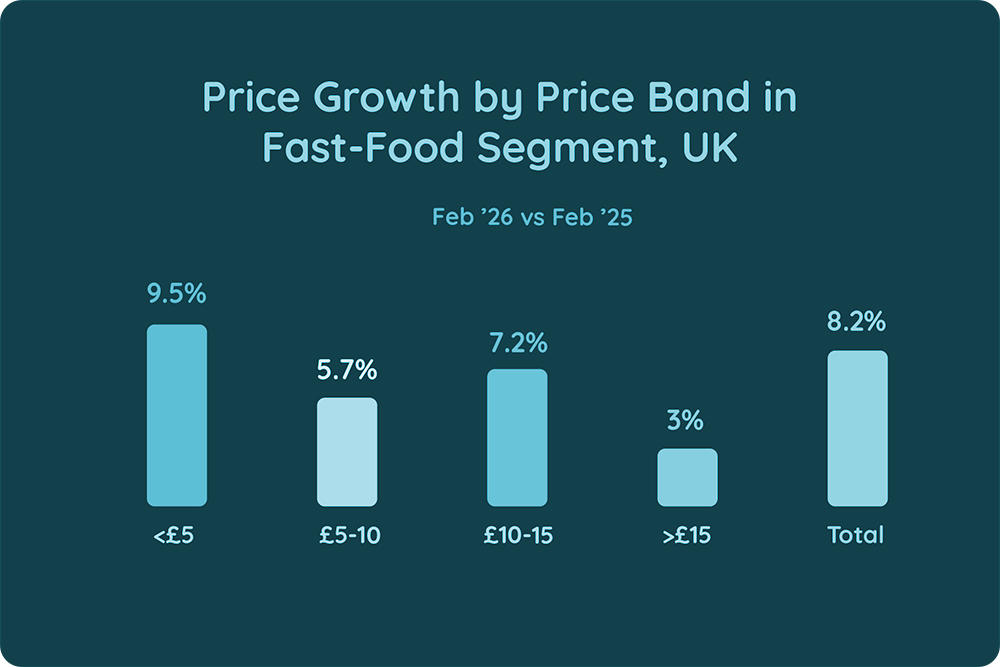

Lower-priced items under £5 saw the sharpest increases, rising from 8.8% to 9.5%, indicating that even entry-level price points are no longer shielded from inflation. Mid-tier products between £10 and £15 also accelerated, climbing from 6.3% to 7.2%, positioning this segment as a key battleground for operators trying to balance margins with customer retention. In contrast, premium items above £15 remained stable at 3.0%, suggesting more limited pricing flexibility at the top end.

Maria Vanifatova, the CEO of Meaningful Vision comments: “As cost pressures persist, customers are more selective, even within fast-food, a channel that has historically benefited from its value positioning. Value menus are becoming more expensive relative to regular items, which impacts the frequency of visits among more cautious consumers. Consumers are becoming more price-aware, and even small increases can influence visit frequency. The brands that will succeed are those that take a more targeted approach to pricing, rather than relying on broad-based increases.”

Looking ahead, the data points to a more challenging environment. Operators will need to move beyond blanket price rises and adopt more precise, data-led strategies that reflect local demand, competitive intensity and customer sensitivity.